Last Unguaranteed Financial Inc. purchased the following trading securities during 2014, its first year of operations: Name Number of Shares Cost Arden Enterprises Inc. 5,000 $150,000 French Broad Industries Inc. 2,750 66,000 Pisgah Construction Inc. 1,600 104,000 Total $320,000 The market price per share for the trading security portfolio on December 31, 2014, was as follows: Market Price per Share, Dec. 31, 2014 Arden Enterprises Inc. $34 French Broad Industries Inc. 26 Pisgah Construction Inc. 60

a. Provide the journal entry to adjust the trading security portfolio to fair value on December 31, 2014.

b. Assume the market prices of the portfolio were the same on December 31, 2015, as they were on December 31, 2014. What would be the journal entry to adjust the portfolio to fair value?

Answer: 2014 Dec. 31 Valuation Allowance for Trading Investments* 17,500 Unrealized Gain on Trading Investments 17,500 Ex. 15–17 a. * $337,500 – $320,000, as determined from the following schedule: Cost Fair Value (Dec. 31, 2014) 1 Arden Enterprises, Inc. ………………………………………………………… $150,000 $170,000 French Broad Industries, Inc. ………………………………………………… 66,000 71,500 2 3 Pisgah Construction, Inc. ……………………………………………………… 104,000 96,000 Total………………………………………………………………………….. $320,000 $337,500 1 5,000 shares × $34 per share 2 2,750 shares × $26 per share 3 1,600 shares × $60 per share b. There would be no adjusting entry for December 31, 2015, if the market prices remained unchanged from December 31, 2014. This is because the unrealized gain from the difference between the cost and market has already been recognized on December 31, 2014. Only changes in market prices would be recognized subsequent to December 31, 2014.

The income statement for Delta-tec Inc. for the year ended December 31, 2014, was as follows:

Delta-tec Inc. Income Statement (selected items) For the Year Ended December 31, 2014 Income from operations $299,700 Gain on sale of investments 17,800 Less unrealized loss on trading investments 72,500 Net income $245,000

The balance sheet dated December 31, 2013, showed a Retained Earnings balance of $825,000. During 2014, the company purchased trading investments for the first time at a cost of $346,000. In addition, trading investments with a cost of $66,000 were sold at

a gain during 2014. The company paid $65,000 in dividends during 2014.

a. Determine the December 31, 2014, Retained Earnings balance.

b. Provide the December 31, 2014, balance sheet presentation for Trading Investments.

Answer: a. Retained earnings, December 31, 2013………………………………………… Plus net income……………………………………………………………………… $ 825,000 245,000 $1,070,000 Less dividends……………………………………………………………………… 65,000 Retained earnings, December 31, 2014………………………………………… $1,005,000 b. Trading investments (at cost)*…………………………………………………… $ 280,000 Less valuation allowance for trading investments…………………………… 72,500 Trading investments (at fair value)……………………………………………… $ 207,500 * $346,000 – $66,000 How to get A+ in Accounting

Highland Industries Inc. makes investments in available-for-sale securities. Selected income statement items for the years ended December 31, 2014 and 2015, plus selected items from comparative balance sheets, are as follows:

Highland Industries Inc. Selected Income Statement Items For the Years Ended December 31, 2014 and 2015 2014 2015 Operating income a. g. Gain (loss) from sale of investments $7,500 $(12,000) Net income (loss) b. (21,000) Highland Industries Inc. Selected Balance Sheet Items December 31, 2013, 2014, and 2015 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2015 Assets Available-for-sale investments, at cost $ 90,000 $ 86,000 $102,000 Valuation allowance for available-for-sale investments 12,000 (11,000) h. Available-for-sale investments, at fair value c. e. i. Stockholders’ Equity Unrealized gain (loss) on available-for-sale investments d. f. (16,400) Retained earnings $175,400 $220,000 j.

There were no dividends.

Determine the missing lettered items.

Answer: a. $37,100 $44,600 – $7,500 b. $44,600 $220,000 – $175,400 c. $102,000 $90,000 + $12,000 d. $12,000 Same as valuation allowance for available-for-sale investments e. $75,000 $86,000 – $11,000 f. ($11,000) Same as valuation allowance for available-for-sale investments g. ($9,000) ($21,000) + $12,000 h. ($16,400) Same as unrealized gain (loss) from available-for-sale investments i. $85,600 $102,000 – $16,400 j. $199,000 $220,000 – $21,000

Hurricane Inc. purchased a portfolio of available-for-sale securities in 2014, its first year of operations. The cost and fair value of this portfolio on December 31, 2014, was as follows:

Name Number of Shares Total Cost Total Fair Value Tornado Inc. 800 $14,000 $15,600 Tsunami Corp. 1,250 31,250 35,000 Typhoon Corp. 2,140 43,870 42,800 Total $89,120 $93,400

On June 12, 2015, Hurricane purchased 1,450 shares of Rogue Wave Inc. at $45 per share plus a $100 brokerage fee.

a. Provide the journal entries to record the following:

1. The adjustment of the available-for-sale security portfolio to fair value on December 31, 2014. 2. The June 12, 2015, purchase of Rogue Wave Inc. stock.

b. How are unrealized gains and losses treated differently for available-for-sale securities than for trading securities?

Answer: a. 1. 2014 Dec. 31 Valuation Allowance for Available-forSale Investments 4,280 Unrealized Gain (Loss) on Availablefor-Sale Investments 4,280 $93,400 – $89,120. 2. 2015 June 12 Investments—Rogue Wave Inc.* 65,350 Cash 65,350 *(1,450 shares × $45 per share) + $100 b. Unrealized gains and losses for available-for-sale securities are accumulated over time and reported as a credit (positive) or debit (negative) balance in the Stockholders’ Equity section. As a result, the changes in fair value are not reflected on the income statement, as is the case with trading securities. Bypassing the income statement is supported on the grounds that available-for-sale securities will be held for a longer time than trading securities; thus, fluctuations in market prices have a greater opportunity to “cancel out” over time.

Storm, Inc. purchased the following available-for-sale securities during 2014, its first year of operations:

Name Number of Shares Cost Dust Devil, Inc. 1,900 $ 81,700 Gale Co. 850 68,000 Whirlwind Co. 2,850 114,000 Total $263,700 The market price per share for the available-for-sale security portfolio on December 31, 2014, was as follows: Market Price per Share, Dec. 31, 2014 Dust Devil, Inc. $40 Gale Co. 75 Whirlwind Co. 42

a. Provide the journal entry to adjust the available-for-sale security portfolio to fair value on December 31, 2014.

b. Describe the income statement impact from the December 31, 2014, journal entry.

Answer: 2014 a. Dec. 31 Unrealized Gain (Loss) on Available-forSale Investments 4,250 Valuation Allowance for Available-forSale Investments* 4,250 * $259,450 – $263,700, as determined from the following schedule: Cost Fair Value (Dec. 31, 2014) Dust Devil, Inc. …………………………………………………………………… $ 81,700 $ 76,0001 Gale Co. …………………………………………………………………………. 68,000 63,7502 Whirlwind Co. …………………………………………………………………… 114,000 119,7003 Total………………………………………………………………………….. $263,700 $259,450 1 1,900 shares × $40 per share 2 850 shares × $75 per share 3 2,850 shares × $42 per share b. There is no income statement impact from the December 31, 2014, adjusting entry. Unrealized Gain (Loss) on Available-for-Sale Investments is reported in the Stockholders’ Equity section of the balance sheet. On December 31, 2014, Unrealized Gain or Loss on Available-for-Sale Investments would be disclosed as follows: Unrealized gain (loss) on available-for-sale investments…………………… $(4,250)

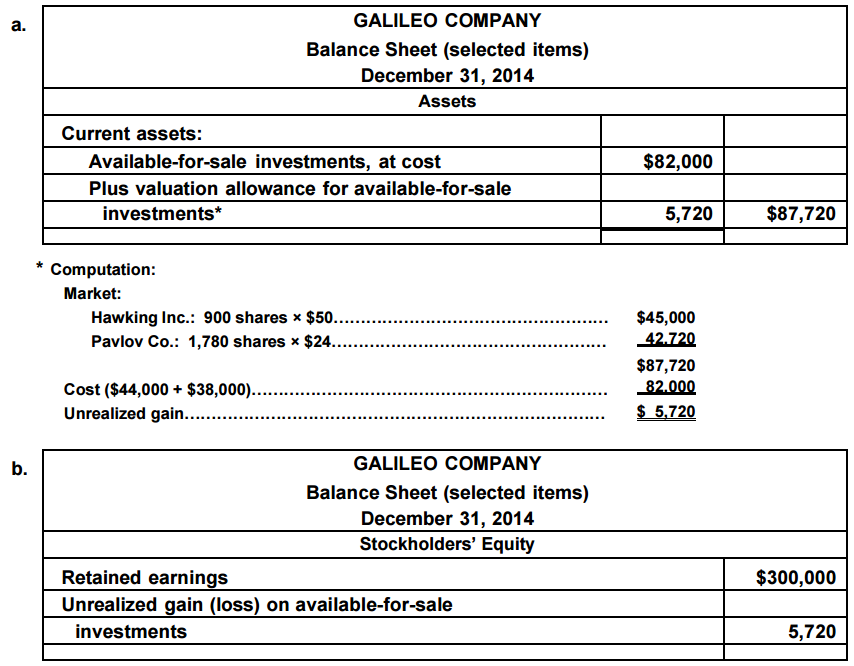

Assume that as of December 31, 2014, the Hawking Inc. stock had a market value of $50 per share, and the Pavlov Co. stock had a market value of $24 per share. Galileo Company had net income of $300,000, and paid no dividends for the year ended December 31, 2014. All of the available-for-sale investments are classified as current assets.

a. Prepare the Current Assets section of the balance sheet presentation for the availablefor-sale investments.

b. Prepare the Stockholders’ Equity section of the balance sheet to reflect the earnings and unrealized gain (loss) for the available-for-sale investments.

Answer: a. GALILEO COMPANY Balance Sheet (selected items) December 31, 2014 Assets Current assets: Available-for-sale investments, at cost $82,000 Plus valuation allowance for available-for-sale investments* 5,720 $87,720 * Computation: Market: Hawking Inc.: 900 shares × $50…………………………………………… $45,000 Pavlov Co.: 1,780 shares × $24…………………………………………… 42,720 $87,720 Cost ($44,000 + $38,000)………………………………………………………… 82,000 Unrealized gain…………………………………………………………………… $ 5,720 b. GALILEO COMPANY Balance Sheet (selected items) December 31, 2014 Stockholders’ Equity Retained earnings $300,000 Unrealized gain (loss) on available-for-sale investments 5,720

At the market close on October 27 of a recent year, McDonald’s Corporation had a closing stock price of $93.49. In addition, McDonald’s Corporation had a dividend per share of $2.44 during the previous year.

Determine McDonald’s Corporation’s dividend yield. (Round to one decimal place.)

Answer: Dividend Yield = Cash Dividends per Share of Common Stock Market Price per Share of Common Stock Dividend Yield = $2.44 $93.49 = 2.6% The market price for Microsoft Corporation closed at $30.48 and $27.91 on December 31, Year 1, and Year 2, respectively. The dividends per share were $0.52 for Year 1 and $0.52 for Year 2.

a. Determine the dividend yield for Microsoft on December 31, Year 1, and Year 2. (Round percentages to two decimal places.)

b. Interpret these measures.

Answer: a. Year 1: Dividend Yield = $0.52 ÷ $30.48 = 1.71% Year 2: Dividend Yield = $0.52 ÷ $27.91 = 1.86%

b. Dividends per share remained constant from Year 1 to Year 2. In addition, the dividend yield increased from 1.71% in Year 1 to 1.86% in Year 2. The increase in the dividend yield is a result of a slight decrease in the stock price. Microsoft provides a small return to the shareholder in terms of a dividend yield and an additional return in terms of price appreciation of the stock.